The outlook for emerging markets

Where to invest beyond developed markets

It is a long time since emerging markets were seen as peripheral investments.

Prominent emerging markets countries, most notably China and India, have been at the vanguard of economic growth and technological innovation.

At the same, they have seen a rapid increase in the consumer sector, with a growing middle class and a desire to develop their own industries, autonomous from the West.

China has been particularly successful, now buying from other Asian countries, and is destined to be the largest economy in the world by the end of this year.

This creates opportunities for investors wishing to develop their portfolio, and expand from their mainstream and more familiar investments.

But there are certain underlying trends in emerging markets that they need to be aware of.

This report sets out some of those challenges and opportunities.

Global funds are the entry point for advisers

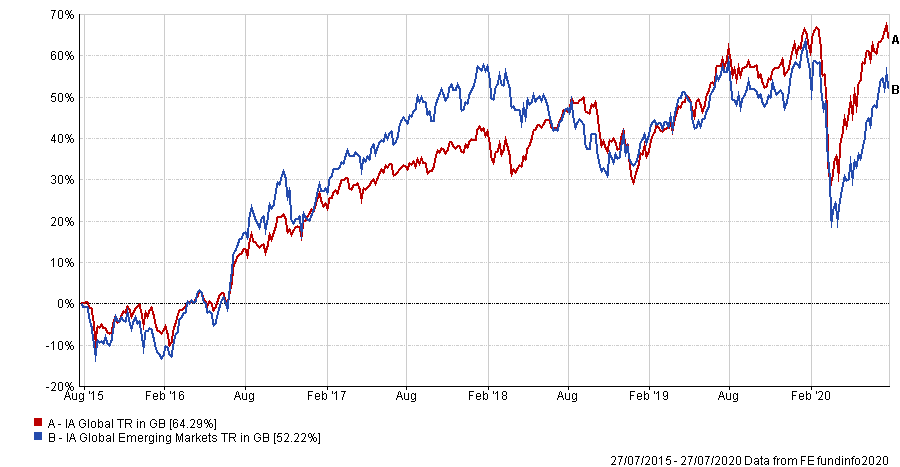

Advisers tend to use global equity funds as a way to invest in emerging markets, according to the latest poll from FTAdviser.

The data shows 68 per cent of the respondents to the poll prefer to access emerging markets via global funds, with only 6 per cent choosing to invest directly in emerging market funds directly.

Data from FE Analytics shows that funds in the IA Global sector have gained 4 per cent over the past year to 6 July, while the average emerging market fund has lost just over one per cent in that time period.

Just over 12 per cent of those advisers said they access emerging markets via regional specific funds.

Emerging markets tend to perform less well in times of global economic uncertainty. This is because US based investors tend to bring their money back home at times of crisis, resulting in dollars leaving emerging markets, making it more difficult for those countries and companies to fund themselves.

But since March, shares listed in China have performed strongly.

Sonal Tanna, emerging market portfolio manager at JP Morgan Asset Management said it is no longer valid to group all of the countries that typically are called “emerging markets” as those economies and stock markets have taken different trajectories in recent years.

Emerging markets after Covid-19

How emerging markets are coping with Covid-19

Throughout history, most economies have taken the same journey, initially being agrarian economies, then, with cheap currencies and low wages, they industrialise as centres for the manufacturing of goods for other people to buy.

Those economies and stock markets which are grouped together by investors as “emerging markets” tend to be at this stage of development.

Investors have traditionally viewed emerging markets as good investment opportunities as this shift means individuals in those economies earn more as they move into industrial employment, boosting demand for consumer goods, particularly for non essential items.

The fund manager Nick Train, who runs the Lindsell Train Global Equity fund, believes the beneficiaries of the rise of the emerging market consumers will be global brands, many of which are listed in developed markets, and which are aspirational purchases.

He cites this as one of the reasons for his various funds having significant amounts of cash in the UK-listed Diageo, a drinks company.

Mr Train believes that as emerging market consumers get wealthier, they will stop drinking “the local firewater” and buy more expensive brands, manufactured by large companies.

This may mean the amount of alcohol consumed goes down, but the profits for alcohol businesses go up.

The journey from being primarily an agrarian economy to a model more focused on manufacturing is one that dozens of countries have embraced in recent decades.

The next, and necessary, stage of the journey for economies is to move out of being mass market exporters, and into being primarily consumption based.

Evolving away from an economic model primarily based on low end manufacturing is necessary due to the realities of currency and interest rate movements, while Phil Smeaton, chief investment officer at Sanlam, says the shift is one that countries also should want to make, as it improves the lives of people.

An emerging economy’s currency rising in value over a prolonged period of time is bad news,

Currency movements matter because, once a country has developed its export base, its currency is likely to rise in value relative to the currencies of the countries buying the exports, as the latter must turn their currency into the currency of the emerging economy in order to purchase the exports.

An emerging economy’s currency rising in value over a prolonged period of time is bad news, as it makes the goods they export relatively more expensive.

Historically, the policy response to this has been to keep interest rates low, as a disincentive to hold the currency.

But low interest rates encourage borrowing, rather than saving, and can lead to a credit bubble emerging, with house prices rising quickly.

This causes a sharp rise in inflation in the economy, and presents policymakers with a dilemma.

The higher inflation will lead to the cost of manufacturing rising in the economy, making them less competitive, while workers will agitate for higher wages.

The 'middle income' trap

Policymakers must either allow the inflation, attempt to drive wages down (which causes the credit bubble to burst) or put interest rates up to curb borrowing, which makes the currency rise in value, and has the same effect in terms of productivity.

Economists call this the “middle income trap.”

It is not unique to those economies classified as “emerging”, the above pattern is precisely what happened in Ireland from the start of the 1990s until the global financial crisis.

Mr Smeaton says moving beyond this export-led model improves the lives of citizens as “they go from making stuff for other people to consume, and start making stuff for themselves to consume.”

Most countries walk blindly into the fixed income trap, with politicians reluctantly to change course early enough, because things seem to be going well, until it is too late.

China has been the exception to this.

Since the global financial crisis, policymakers in that country have pursued policies to move the country to consumption based growth, and escape the middle income trap.

This has resulted, according to Gero Jung, chief economist at Mirabaud, in China exporting more high value goods.

This escapes the middle income trap, because the economy is not required to be the cheapest producer, with a cheap currency and low wages if it is selling goods that are expensive, and advanced, such as technology products.

Chinese workers earning salaries for work on high value added goods are now buying the cheaper goods from countries embarking on the journey now that China was on 30 years ago, of being the manufacturer.

Alastair Way, emerging markets fund manager at Aviva Investors, says the net effect of this is the fate of the Chinese economy is now more important than the outlook for the US economy, as China consumes many of the commodities and manufactured goods made in other emerging markets.

Chinese workers earning salaries for work on high value added goods are now buying the cheaper goods from countries embarking on the same journey

Justin Leverenz, emerging markets equity fund manager at Invesco, says it is increasingly the case that emerging markets are “China plus the rest”, both in terms of the relative size of the stock market and the impact of the Chinese economy on the rest.

Mr Jung says he is “optimistic” about the outlook for the Chinese economy.

He says: “There are advantages to being the first into the pandemic and the first out.

“One of the issues China has as an economy is that its demographics are terrible, it has an ageing population, and that usually slows down growth.

“But China has responded to this by being very productive, and making higher value goods. Because I am quite optimistic on China, I am bullish on the emerging Asia economies in general.”

Gael Combes, head of fundamental research at Unigestion, said a situation is developing in emerging markets whereby the local companies are much stronger than the international competitor, making accessing emerging market growth via companies listed in developed markets less attractive in his view.

He adds that the trade disputes between the US and China is likely to quicken the pace of other Asian economies moving from agrarian to industrialised economies, as businesses try to avoid tariffs.

The All Mighty Dollar

Away from economic fundamentals, the traditional main driver of asset prices in emerging markets is the dollar.

This is because, whether they are close to reaching the middle income trap or not, most emerging market countries and companies are only able to borrow in dollars.

This makes those stock markets acutely vulnerable in volatile times, as if US investors want to reduce the level of risk in their portfolios, they tend to sell their overseas assets and bring the cash home.

This means cash is dragged from emerging market assets, almost regardless of the fundamentals, and so those asset prices fall.

Mr Way says this correlation between the dollar and emerging market equities has weakened in recent years, particularly as China has become a bigger part of the index.

He adds: “Demand for western goods is still strong in emerging markets, but what you get in emerging markets is the platform.

“So they might want Unilever goods, but they buy them online via a local site.”

Demand for western goods is still strong in emerging market but what you get in emerging markets is the platform

Mr Leverenz says emerging market assets are likely to benefit from the low interest rates policies implemented in the US in response to the pandemic.

“Low interest rates act as an incentive for US investors to put their capital to work overseas in search of a higher return, while overseas investors are rendered less likely than in the past to put their cash into US government bonds, helping to keep a peg on the value of the dollar.

Selecting EM investments

Freddie Woodhead, investment manager at wealth management firm JM Finn believes emerging market equities are suitable to be held in the portfolios of clients across the risk spectrum.

He says: “There are three ways to invest in emerging markets, the first is via global equity funds with significant allocations to emerging markets, the second is to dedicated emerging market funds and the third to regional funds.

“We would not tend to do the third of those very often, we would say let the manager show their expertise by picking the region.

“The largest investment across all portfolios at JM Finn is the Scottish Mortgage investment trust, which has significant holdings in emerging markets. We would only do region specific funds if the client requested exposure to a particular theme.”

He added that he tends to move between the growth and value styles of investing in emerging markets depending on his outlook. He said the value stocks tend to have more of a dividend yield, which makes them suitable for some clients more than others.

Kiran Nandra, product specialist for emerging markets at Pictet, says corporate governance remains an issue in many emerging market companies, and should be a major focus for emerging market investors.

She says that while standards have improved in recent years, it continues to be something investors need to be wary of.

Ms Nandra says: “The only way to do this is to go out on the ground and see what is happening.

“One example we would have is we were invested in an emerging market bank, and we mystery shopped in the bank to see what would happen. We asked for a loan, and they offered us a loan amount way higher than is prudent and that was a red flag for us.”

Gordon Fraser, manager of the BlackRock Emerging Markets fund says he believes Indian and other Asian equities will perform better in the months to come.

At the start of the year, Mr Fraser reduced the level of risk in his portfolio, as he believed the market was underestimating the chances of a recession.

But the pandemic has, he says, unleashed waves of liquidity into global markets, and this should boost emerging markets in the medium term.

Five reasons to use an active fund manager in emerging markets

Many investors are attracted to emerging market companies for their high growth and investment returns potential.

For those investors comfortable with the higher risk that accompanies this, the next question is how to invest in these countries.

This could be via a typically lower-cost, market-tracking product such as a passive fund.

Or they could pay more and use an active fund manager, with the potential to receive a return above that of the market average?

In emerging markets in particular, we think that there is a strong case for using an active manager.

1. Emerging market active fund managers can capitalise on index evolution

The opportunity set - that is the countries and companies in the index - for an emerging market equities investor is constantly evolving.

It has changed dramatically over the last 30 years, as developing countries have opened their markets to foreign investors, and improved their operational and regulatory regimes.

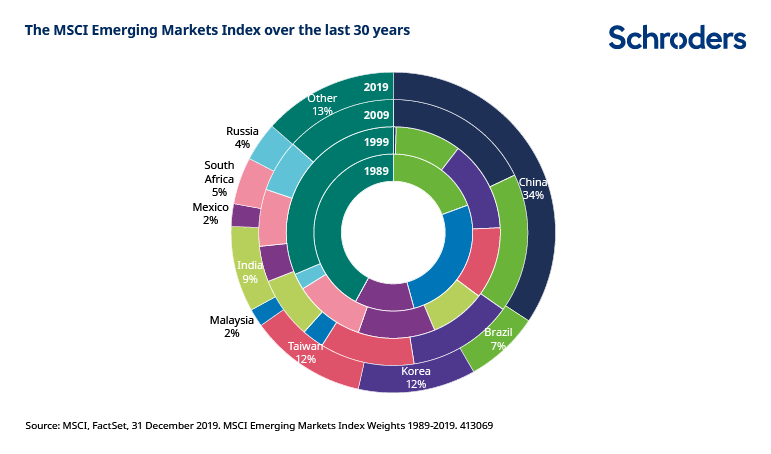

The chart below shows how the MSCI Emerging Markets Index has changed over this period.

The biggest change is China, which has gone from zero to 36% at the end of 2019 (at the time of writing China’s share of the index has risen to over 40%, due to index changes and year-to-date market performance), whilst Latin America’s weight has shrunk by over 20%.

You can read more detail on the changes in the article we wrote back in 2018.

Kuwait will be added to the MSCI Emerging Markets Index in November this year, while MSCI is currently consulting with investors on whether to continue Argentina’s inclusion.

Why is this important?

With the potential for future evolution, active investors’ ability to anticipate benchmark changes and invest outside the index is valuable.

It can enable active fund managers to identify and take advantage of attractive investment opportunities ahead of passive funds.

What this often means in practice is that active funds can enter a market in advance of its inclusion in the index.

These events are well-flagged by index providers such as MSCI, and active funds, unlike index-following products, are usually free to invest at a time they view attractive, rather than from a specified date.

2. Retail investor dominance

Although not always the case, institutional investors typically have greater time and resources to dedicate to asset valuations, and trade on information and set prices.

Conversely, retail investors do not usually have the same means to conduct company research, and in some cases asset valuation is not a part of their buying and selling decisions.

A higher share of informed investors in a market makes that market more efficient and reduces the opportunities for active investors.

We can use the market share of institutional investors as a rough proxy for the market share of informed investors.

In the chart above, we show the percentage participation of institutional investors in a range of global equity markets.

The share of institutional investors, both international and domestic, is on average lower in emerging equity markets than it is in the US and other major developed markets, and in some instances, such as China, very much lower.

It is not therefore simply the amount of change in emerging market indices that makes emerging markets a more favourable environment for active managers than the more stable developed markets.

The higher share of retail participants in emerging stock markets should be positive for fund managers with robust investment processes based on fundamental research.

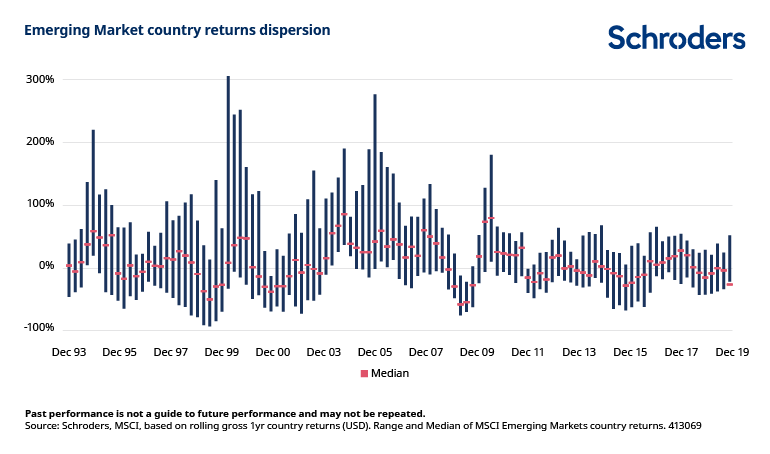

3. The performance of different countries and stocks varies greatly – this provides opportunities

An important point to make is that the description “emerging”, relates to the stock market as opposed to the country.

Emerging market countries are in fact highly diverse and at very different stages of development.

They include Qatar, where GDP per capita is higher than in the US, through to Pakistan where GDP per capita is around one fiftieth of that in the US.

Partly as a result of this diversity, the spread of returns from countries and stocks has been persistently wide. The chart below shows the dispersion of one year returns for the countries in the MSCI Emerging Markets Index, going back to 1991, highlighting the median average return. Although the range has reduced since the financial crisis in 2008, there is still a wide spread between the best and worst performing countries (the height of the blue bar).

This potentially creates opportunities for active managers to generate returns in excess of the market average. This can be achieved by holding a higher exposure of their fund than the index to countries and stocks which perform better than the market, and by maintaining a lower exposure to, or avoiding altogether, those which underperform.

Furthermore, many of these markets are under-researched in comparison to developed markets.

This provides the opportunity for a fund manager and team of analysts to uncover attractive investment opportunities before these are reflected in market prices.

Of course, as we mentioned at the outset, investment in emerging markets is higher risk and returns can be more volatile.

4. Better integration of environmental, social and governance issues

Environmental, social and governance, or ESG, concerns are more important today than ever before, and these are particularly significant in emerging markets.

Company disclosure in emerging markets is, in some cases, poor and regulation may be less stringent.

Corporate governance standards vary widely. Meanwhile minority shareholders can be a lower priority, which often translates to weaker share price performance.

We think that fund managers are able to gain an edge on index tracking products, by integrating ESG considerations into their investment process. By meeting with companies, fund managers can better understand the issues that they face, and how they are managing them.

Some products which track an index often try to filter out companies which do not meet certain ESG standards. However, these methods are usually backward looking, dependent on the quality and consistency of data, and do not place any value on engagement with companies.

Third party companies provide ESG ratings, but there is little consistency between different providers.

One factor behind poor governance standards is the prevalence of state-owned enterprises (SOEs).

SOEs account for more than 20% of the companies in the MSCI Emerging Markets Index, compared to less than 1% in the MSCI World.

These are companies which are publicly listed, but in which the state has a controlling share; the government can appoint management and dictate how they are run.

In SOEs, controlling shareholders interests are not always aligned with those of minority shareholders. An active manager can benefit by anticipating periods when interests are or are not aligned. Most index tracking products, by contrast, would hold exposure to these companies at all times.

5. The performance of active funds versus trackers in emerging markets is favourable

Data from Copley Fund Research shows that over the five-year period ending December 2019, around two-thirds of active managers outperformed the passive products that most investors can access, net of institutional management fees.

This is based on a sample of 222 actively managed global emerging market equities funds with a combined $350 billion in assets under management.

However, it is not always plain sailing right from the start.

You need to hold a fund for more than a year, and preferably up to three years, before it starts to outperform reliably.

(The exception to this was the global financial crisis when active managers underperformed, and took a long time to recover.)

An investor needs to have conviction that a manager’s investment process can deliver above market average returns, and confidence that the manager is sticking to that process.

Indeed, the fund selection challenge needs to be reframed. Rather than trying to pick the top-performing fund, institutional investors should try to avoid the worst performing funds, which is potentially a much easier task.

Of course, retail investors pay higher fees, which reduces active funds’ net performance versus index following alternatives. However, the higher fees do not propel index trackers convincingly into the top half of performers. As an example, a US retail investor choosing an active emerging markets fund at random would have outperformed a market tracker alternative roughly half the time over the past five years.

Another point to be made is that although retail investors do not have direct access to managers to conduct due diligence, they do have indirect access if they go through an intermediary who undertakes manager research on their behalf.

For retail investors, despite the higher fees and with some due diligence, it can still make sense to choose an active manager in emerging markets. Particularly in an environment where any outperformance can be a significant portion of the overall return.

Kirsty McLaren is investment director, emerging market equities at Schroders

Important Information:

Reliance should not be placed on any views or information in the material when taking individual investment and/or strategic decisions. This is not a recommendation to buy or sell any financial instrument/stock or to adopt any investment strategy.

Investments concentrated in a limited number of geographical regions can be subjected to large changes in value which may adversely impact the performance of an investment

Please be aware the value of investments and the income from them may go down as well as up and investors may not get back the amounts originally invested. Past performance is not a guide to future performance and may not be repeated.